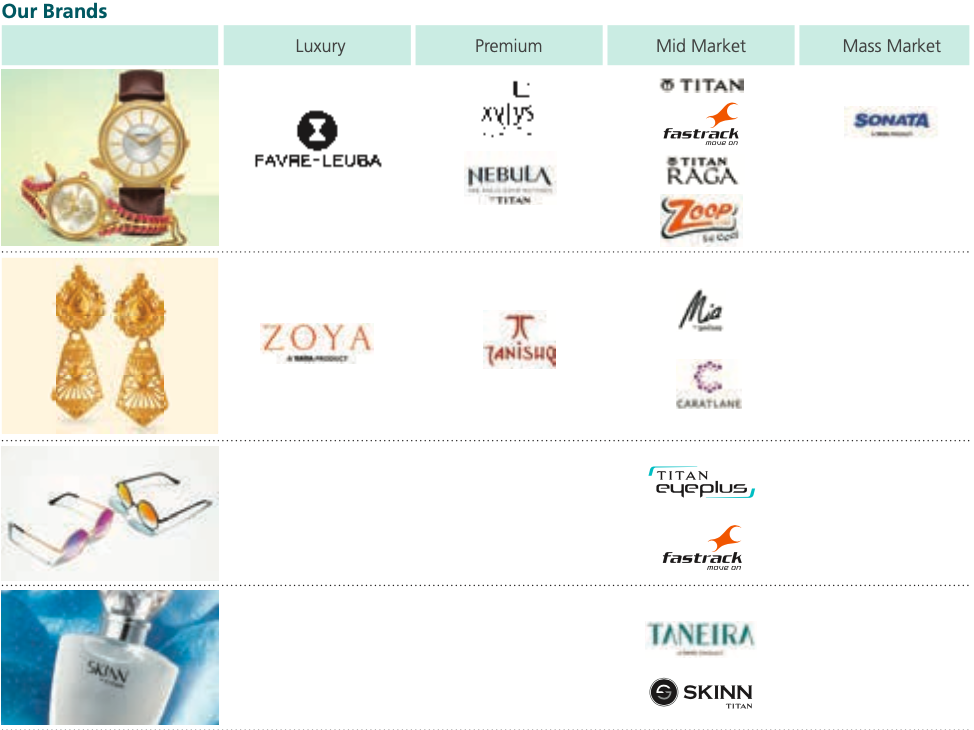

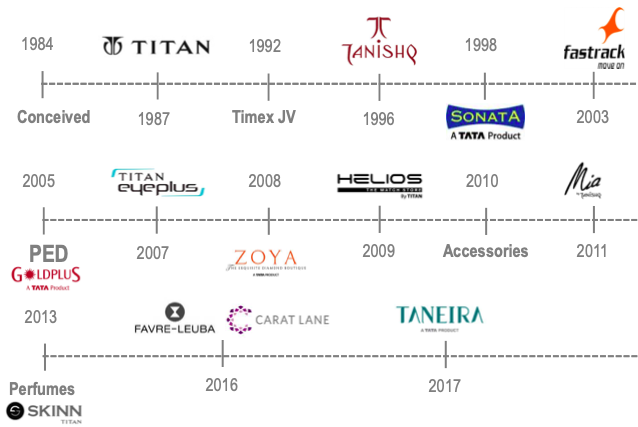

Titan was established in 1984 as a JV between Tata Group and Tamilnadu Industrial Development Corporation (TIDCO). It started with watches, then in 1996, it moved on to jewelry, and in 2007 it entered the eyewear segment. It has a strong connection with its consumers through its multi-brand portfolio.

Titan is India’s most successful consumer brand. It successfully transitioned from being a watch only company to a lifestyle player with multiple brands. Today, its jewelry segment generates 83% of revenue and 88% of profits. Watches generate 12% of revenue and make 12% of profits. Eyewear and other segments generate 5% of revenue and no profits.

Its playbook is simple: build great products and brands in underserved, underpenetrated, and unorganized categories. It entered sectors with poor business practices and ethics and made it win-win for everyone.

What are the competitive advantages of Titan?

Ability to create new brands and generate demand: Before Titan came onto the scene, HMT and Allwyn are the only watches available legally in India. A watch was considered a lifetime purchase. You buy one and keep it forever. Titan offered more reasons and encouraged ownership of multiple watches.

Titan observed that people were gifting watches to friends and family on significant occasions in their lives. It capitalized on this finding through ads focusing on the emotions of gifting a Titan watch. Do you remember this Titan ad of a father gifting a watch to his daughter with Mozart’s 25th Symphony background music?

Jewelry is still seen as an investment in India. Titan is changing this perception and made Tanishq a strong adornment brand. Consumers are willing to pay more than one crore for its jewelry and buying for adornment than investment. Tanishq brand gives it strong pricing power. In the last decade, it has been earning a 26-28% gross margin. It makes a 3-4% pricing premium compared to peers in the same area of operation. Studded gold jewelry sales are growing faster than plain gold jewelry, which is good for Tanishq as it’s margin accretive.

Titan knows how to create new product categories and sub-brands within a category to cater to the needs of different demographics. For example, Tanishq is a jewelry brand. Caratlane is an online jewelry brand. Mia is an affordable jewelry brand. Zoya is a high-end jewelry brand. In the last 25 years, it has created over a dozen successful multi-million dollar brands.

Trust, Focus on win-win, and Asset light business model: What is 22 karat gold? It is gold containing 91.6% gold and 8.4% alloys. In the absence of hallmarking, many jewelers claimed they were selling 22 karat gold, but sold lesser karat gold. They made more margins by screwing their customers.

Tanishq installed Karatmeter in stores that used X-rays to measure the purity of gold in three minutes, exposing the unfair practices of family jewelers. It ran an ad telling that, “There’s a thief in the family.” Tanishq’s transparent way of doing business increased customer trust, resulting in the share of gold exchange rising to 40% from 15% in 2013.

Around 95% of the investment required to set up a jewelry store goes to inventory. There are three ways a jeweler can source gold (a) exchange from the customer, (b) lease it from banks, (c) buy from the spot market. Exchanging from the customers is cheap as you don’t need to hold inventory, and usually, a customer purchases more than what they exchange for.

It is expensive to buy gold from the spot market as capital gets tied to inventory and the jeweler gets exposed to the risk of gold prices going down. It is efficient to lease gold from banks by paying 3-4 percent annual interest. You reduce working capital and not worry about gold prices going down. Banks don’t have any problems leasing gold to trusted players like Tanishq.

The new generation of karigars (craftsmen) is more inclined to work for Tanishq as they provide better salaries, food, accommodation, and other facilities such as schooling for their children. In contrast, unorganized players have a long history of exploiting these karigars. Tanishq follows the advice of Richard Branson — Take care of your employees, and they’ll take care of your business. It’s as simple as that. Healthy, engaged employees are your top competitive advantage.

Even in the eyewear retailing, unorganized players were following unfair practices. For example, unbranded frames got sold as branded frames. There was no transparency in lens prices, and customers didn’t know if they were paying fair prices. Titan Eyeplus entered the market using trust and transparency. It didn’t upsell expensive products to customers. It replaced its target metrics to make it more customer-friendly.

From the beginning, Titan adopted the franchisee model to scale fast and develop an asset light business model. In the book Titan: Inside India’s Most Successful Consumer Brand, Vinay Kamath writes:

Titan proactively attracted business persons from outside the watch trade to set up watch shops even if they needed extra help to do it. Partly because there were no middlemen, Titan could also offer better margins to retailers. ‘All these policies served us well in the initial years; they were the key to maintaining low working-capital borrowings and enabled us to show profits from the very first year of operations’

Titan’s playbook is to develop the brand and take the franchisee route to scale it. The franchisor must have a strong brand and be trustworthy for franchisees to sign up. Titan has both brand and trust, giving it an asset-light business model and high ROCE.

| Company | Sales | EBITDA Margin | ROCE |

| Titan Jewelry | ₹16,390 | 12% | 62% |

| PC Jewellers | ₹8,672 | 8% | 18% |

| TBZ | ₹1,764 | 4.5% | 7% |

Capacity to suffer and continue to invest for the long term: I like management that’s willing to look stupid in the short term to build a durable franchisee in the long term. Eyewear business sales grew at a decent rate of 23% in FY19. But even after a decade, it didn’t generate any profits. Why is that?

Its eyewear business has high gross margins. It is investing significantly in marketing to build the brand, resulting in diluting the profit margins in the short term. In the recent investor forum, the management said:

Margins will come, we have mentioned this so many times, margins will come. Just like in Jewellery when we talk about the fact that forget margins, we will grow, we will take the opportunity, we are doing the same thing in Eyewear. So Eyewear, I am sure we will get our margins, it is just that now we are deliberately investing more in advertisement.

What can disrupt Titan?

Government policy changes: The current account deficit (CAD) happens when a country imports more than its exports. The two biggest import items responsible for India’s CAD are oil and gold. Oil is an essential item, whereas gold isn’t.

In the past, India placed several restrictions on gold imports to keep CAD under control. For example, the 80:20 import rule required only 80% of the imported gold to be sold domestically, and the remaining 20% to be exported. In the past, RBI tried restricting companies to lease gold from banks. We can’t remove the risk of government policies impacting the prospects of the gold industry and Tanishq.

Changing taste of millennials and lack of interest in gold jewelry: The younger generation doesn’t fancy gold jewelry as much as their parents. Tanishq is aware of millennials changing tastes and has created brands like Mia, fashioned for the woman who looks to jewelry to express herself.

Weddings account for 50% of jewelry sales. It’s not just the bride and bridegroom, but their entire family buys jewelry before the wedding. If millennials prefer simple weddings with fewer invites, then growth can be muted.

Other risks: Jewelry sales have a high ticket size. So online sales above 25k rupees are rare. Also, Titan owns CaratLane, which sells jewelry online to tap into the increasing trend of digital shopping.

Customers have the option of renting jewelry from players like Eves24.com. They have to pay a rental fee of 3% of the value, and besides that, they have to pay a deposit that is equal to the jewelry’s value. Given the high cost, I don’t see rental players disrupting Tanishq.

It will take a minimum of 12-18 months before we find vaccines to immunize us from COVID 19. Until then, it’s unclear if the Indian economy will come back to its previous highs. Demand for discretionary lifestyle items will remain muted.

Many of the Tanishq stores are located in malls and high-streets, so adherence to social distancing norms will impact Tanishq’s sales. Time will tell how Titan and its franchisees navigate the turbulent times. If there’s one thing that will help Titan, it’s its debt-free balance sheet.

How to think about the valuation of Titan?

Jewelry segment has a lot of tailwinds for organized players like Titan. Demonetization, GST, cash limit on purchases and mandatory hallmarking will make life hard for unorganized players. With single-digit market share in all lifestyle segments, Titan will gain market share and grow its revenue at double digits seems reasonable.

At the current price of 850 rupees, Titan is selling at 3.5 times TTM sales and 39 times normalized profits. COVID 19 will negatively impact sales and profits in the near term. If Titan can grow its topline at 15%, the expected IRR over the next ten years will be around 12-13%. The key question to ask is can Titan come out stronger after COVID 19?

| Revenue | ₹21,229 | Tax rate | 25% | Cash + Invest | ₹1,100 | Current value | ₹75,302 | |||

| Growth rate | 15% | Reinvestment | 60% | FCF | ₹17,845 | Future value | ₹250,829 | |||

| Operating Margin | 12% | Exit Multiple | 30 | Terminal value | ₹231,884 | IRR | 12.8% |

References

- Titan investor relations

- Titan: Inside India’s Most Successful Consumer Brand

- The man behind Titan’s success

- Investor Diaries by Jatin Khemani

- Demystifying Titan Company

- Several brokerage reports

Disclaimer: I own shares of Titan. This is not a recommendation to buy, sell, or hold. I am not a SEBI registered analyst. I wrote this document to organize my thoughts and deepen my understanding of the company and the industry. I am sharing it so that you can learn something from this.

Thanks for the analysis. On screener, I see Net Cash Flow “Rs. -43 crore for Mar 2019 and Rs. -209 crore for Mar 2018”. However, you mentioned “FCF as Rs. 17,845” as above. Could you please help me understand how you derived at it?

FCF in my table refers to the sum of free cash flows that Titan will generate over the next ten years. This is different from the net cash flows you are referring to. One day I write a post of how I calculate the IRR.

Regards,

Jana

Thanks Jana

REGARDS Dr.R.V. Murali

>

Enjoyed reading this, currently with a PE of 50 it is trading more than its 5 year pe (47) and 10 years pe(40) as per screener. My personal opinion is if we can get it below the 10 year pe then it will be good value.

Would love to know your thoughts on this

It has been one of the great read that i have experienced. Simplicity in writing made it awesomw

Good stuff Jana.

Excellent writeup.I beleive you have not accounted for the saree business they would embark on.i had heard this sometime earlier in an management interview. I am not sure if that is put on hold or cancelled.

Taneria doesn’t generate any profits today. It has a lot of potential in the future, if executed well. I am assuming that Titan will continue to grow at 15% over the next ten years, also helped by Taneira.

Hi Jana,

Can you please tell why did you mention 30x as exit multiple. Maximum exit P/E you should accord to a high-quality business is 20x. Correct me if wrong.

If Titan continues to grow at decent rates beyond ten years with high ROCE, then P/E of 30 should be ok. Another way to look at is future price-to-sales ratio, which comes to 2.9x in the 10th year.

Hello Jana,

I just wanted to know how to came at that valuations. My worksheet doesn’t match yours. Please share it for educational purpose please…

Thanks Jana for an excellent one again.

I am new to your blog.Pl send a brief explanation about the Table in the end arriving at IRR,as I could not understand.Thanks

Sent from my iPad

>

In a normal DCF, you would discount profits from each year at some discount rate, add them up, and arrive at intrinsic value. Then compare the intrinsic value with the current price and decide if it’s worth a buy.

The challenge I have with that is to do some more work to arrive at the IRR. My model still uses DCF. However, I directly calculate the IRR using the current market capitalization and expected market capitalization after ten years.

To see it yourself, run the usual DCF with the above assumptions at a 10% discount rate. You will see that the intrinsic value will be above the current stock price. That’s why the IRR is ~12.8%.

If the intrinsic value is the same as the current stock price, then the IRR will be 10%, the same as your discount rate. If the intrinsic value is below the current stock price, then the IRR will be lower than 10%

Regards,

Jana

Reblogged this on Site Title.