Tamal Bandyopadhyay is a prolific writer, has a knack for explaining difficult banking concepts using simple words. If you’re interested in learning about HDFC Bank, then I highly recommend his book A Bank for the Buck. Recently, I read his book From Lehman to Demonetization, which gives the lay of the land of what happened in the Indian banking industry from 2008 to 2016. I learnt a lot about different shades of NPA, which I am summarizing it in this post.

In March 2012, public and private sector banks in India had lent out 48 trillion rupees. Asset quality appeared to be reasonable based on the reported gross NPA (2.8%) and net NPA (1.3%). There was one problem. Gross NPA only tells half the story. To get the full picture of the asset quality, along with gross NPA, we need to look at restructured assets and write-offs.

Banks are in the business of giving loans to individuals and companies. Some of its customers will not pay interest or principal for some time due to harsh business conditions. If customers don’t pay interest or principal for more than 90 days, then banks will classify these loans as non-performing assets (NPAs).

Once a loan becomes an NPA, a bank is required to set aside money to cover potential losses. It reduces profitability and limits a bank’s ability to lend more.

Loans that are written off are removed from the bank’s balance sheet but parked at the branch level. When some part of the loan gets recovered, it is added back to the profits.

Restructuring, also known as recasting, helps avoid a loan becoming an NPA. How does restructuring work?

- Bank can give a new loan to tide over the current cash flow problem.

- It can give a moratorium on the payment of interest and principal.

- It can reduce interest rates.

Restructuring is a global phenomenon, pioneered by Bank of England in the 1970s. It is a win-win for both the bank and the borrower. For banks, the asset quality stays pristine. For borrowers, they get more time to pay back their dues. It works if the borrower is genuinely interested in paying back the loan.

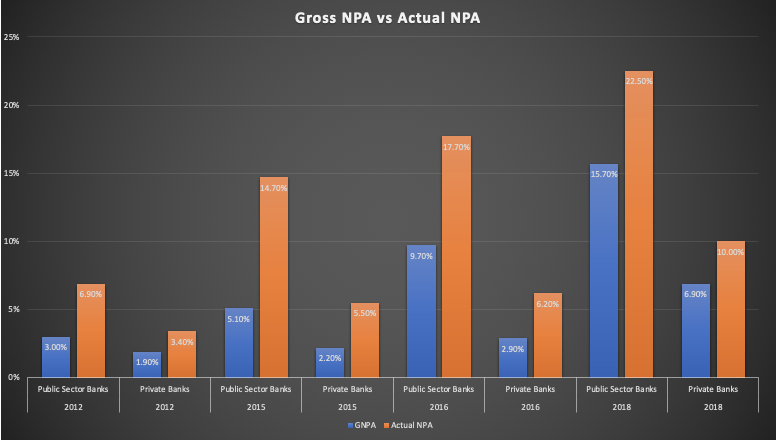

Is restructuring of loans working for Indian banks? Spend time reflecting on the chart above. What do you see?

From 2012 to 2015, the actual NPA (gross NPA + restructured loans + write-offs) for public sector banks shot up from 6.9% to 22.5%. Also, from 2015 to 2018, money lent out by public sector banks didn’t grow at all. Loan restructuring has done more damage to Indian banks.

Uday Kotak, managing director of Kotak Mahindra Bank, doesn’t like restructuring as a philosophy. He tells:

We don’t like restructuring as a philosophy, so we’ve always been very conscious and conservative about doing restructuring. We would rather take it, and take the pain through NPL and get our recoveries… First on let me just give you again something which is on philosophy which is important. If we have to restructure a loan, as long as we are not going to lose our money, we are comfortable making an NPA and then restructuring as a philosophy. And therefore, if you look at our restructured standard loan it is the lowest in banking. And that is coming again out of a view that much rather restructure after taking it through the NPLs if we have to. And of course, it is not that we don’t restructure just for the heck of it. Because when you take a loan to an NPA, your provisioning is much higher than a restructuring, number one. Number two is in a restructuring you continue to accrue interest. In an NPA, you stop accruing interest as well as reverse the accrued interest. So both these from a revenue and P&L point of view are significantly different from a standard restructured loan but we are happier to do that because at least we know what are the things we really need to focus on and get on with, trying to get fair value of that asset. – Uday Kotak

It’s easy to grow a loan book at high double-digit rates. All you need to do is to lend money without worrying about the creditworthiness of your borrowers. However, it takes a lot of intelligence to grow a loan book with quality. Banks report their NPA to show how well their loans are performing.

The only problem with NPA is the management discretion that goes into calculating it.

During good times everyone reports low NPAs. It’s hard to figure out who is swimming naked and who isn’t. The best way to find out is to time travel and see which banks didn’t change their NPAs much when their books got audited by the RBI.

In 2015, Raghuram Rajan, former RBI governor of India, decided to clean the balance sheets of all commercial banks. After inspecting their loan books, RBI asked all the banks to make three kinds of provisions:

- NPA that were earlier not recognized by them.

- Loans given to various projects, where the dates of commencement of commercial operations have passed, but the projects have not yet taken off.

- Restructured loans.

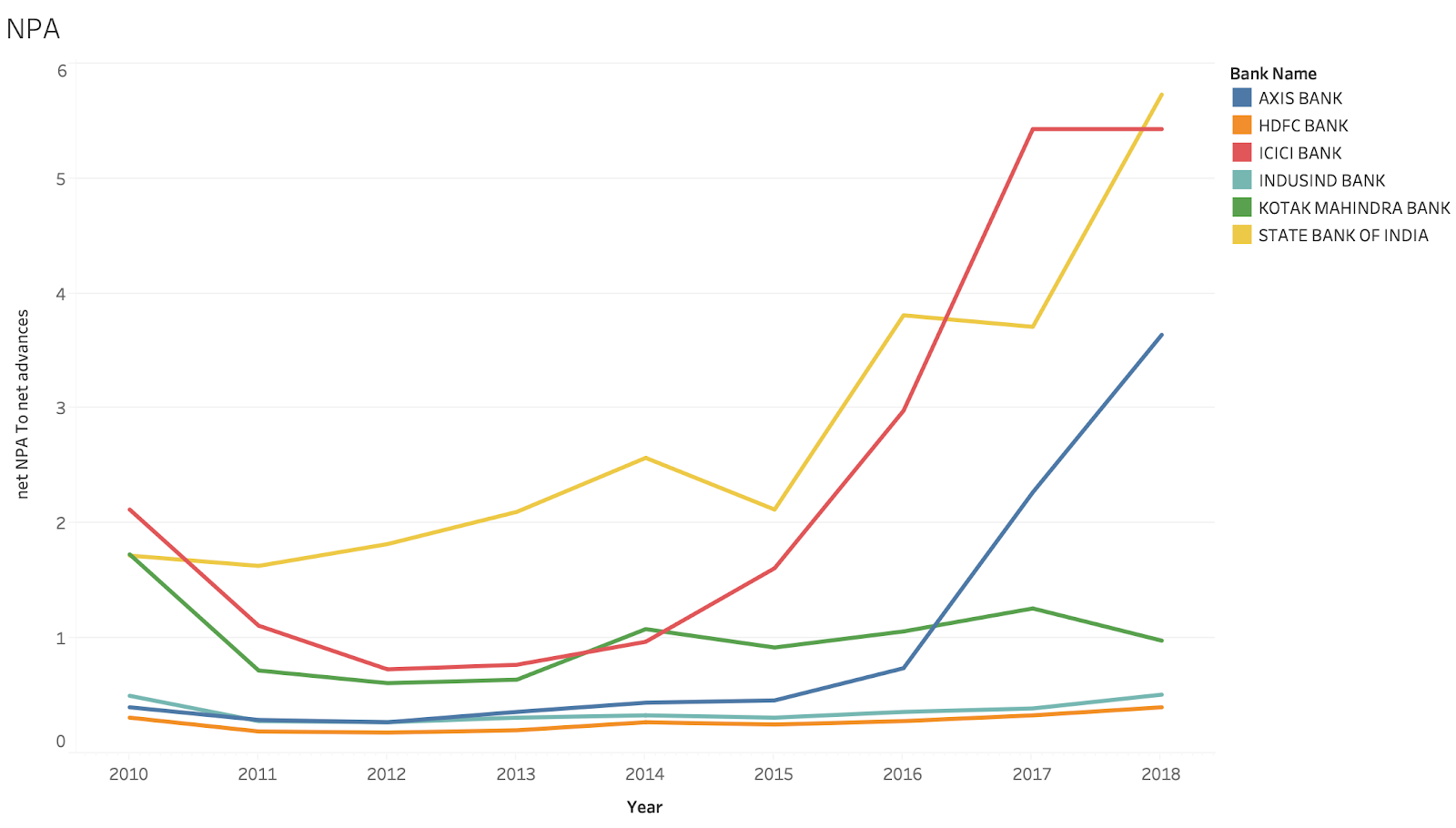

Banks have been playing the game of loan restructuring for a long time without showing these loans as non-performing. Of the six banks I looked at, HDFC Bank, IndusInd Bank, and Kotak Mahindra Bank came out well.

Our andhrabank 6crore rupees msme loan account declared npa on 21-01-2019 iam requested to banker pls make my account asper 1-01-2019 rbi circular meaningful restructuring they are violated rbi guidelines and implemented sarfaesi proceedings what can i do

This is a really insightful post Jana. Do the banks report restructured assets in their Annual report?

I think they should. You can pull the information from the RBI website: https://dbie.rbi.org.in/DBIE/dbie.rbi?site=publications#!4

Regards,

Jana

Great post Jana! This nuance about NPA is something that every investor should understand especially those who invest in banking stocks.

Thanks, Anshul.

Regards,

Jana

I heard something interesting about the interest cost from the Planet MicroCap Podcast, https://www.podbean.com/eu/pb-zyg56-c91798 (Ep. 101).

Let’s say there are two banks, Bank A and Bank B. Let’s say Bank A source “x” amount of deposits through its physical locations, Bank B sources “2x” (or > “x”) amount of deposits from the same or lesser number of physical locations. Given everything else is the same, Bank B will always earn and compound more over time and has a higher degree of competitive advantage over Bank A. You might already know this, but I just came to be aware of this insight 🙂

Thanks, Raghu for sharing. Yes, all else being equal, sourcing customers at a lower cost is indeed an advantage.

Regards,

Jana